2026.07.09

Carlos Ruiz del Vizo

Insights from our recent webinar with Trevor Loy, Founder and Managing Partner of Flywheel Ventures; Adjunct Lecturer, Stanford University; and longtime faculty member and subject matter expert for VC Unlocked: Silicon Valley.

AI is eating venture capital. Last year, 61% of global VC investment went into AI companies, up from 30% just three years earlier. Revenue ramps are compressing, valuations are climbing faster than ever, and capital is concentrating at the top in ways the industry has never seen.

So does any of the old portfolio construction playbook still apply?

The honest answer is mixed. AI is changing the inputs to portfolio construction, but the fundamental laws governing venture returns remain firmly in place (at least so far). Here's what every VC fund manager, especially emerging managers, should understand about both sides of that equation.

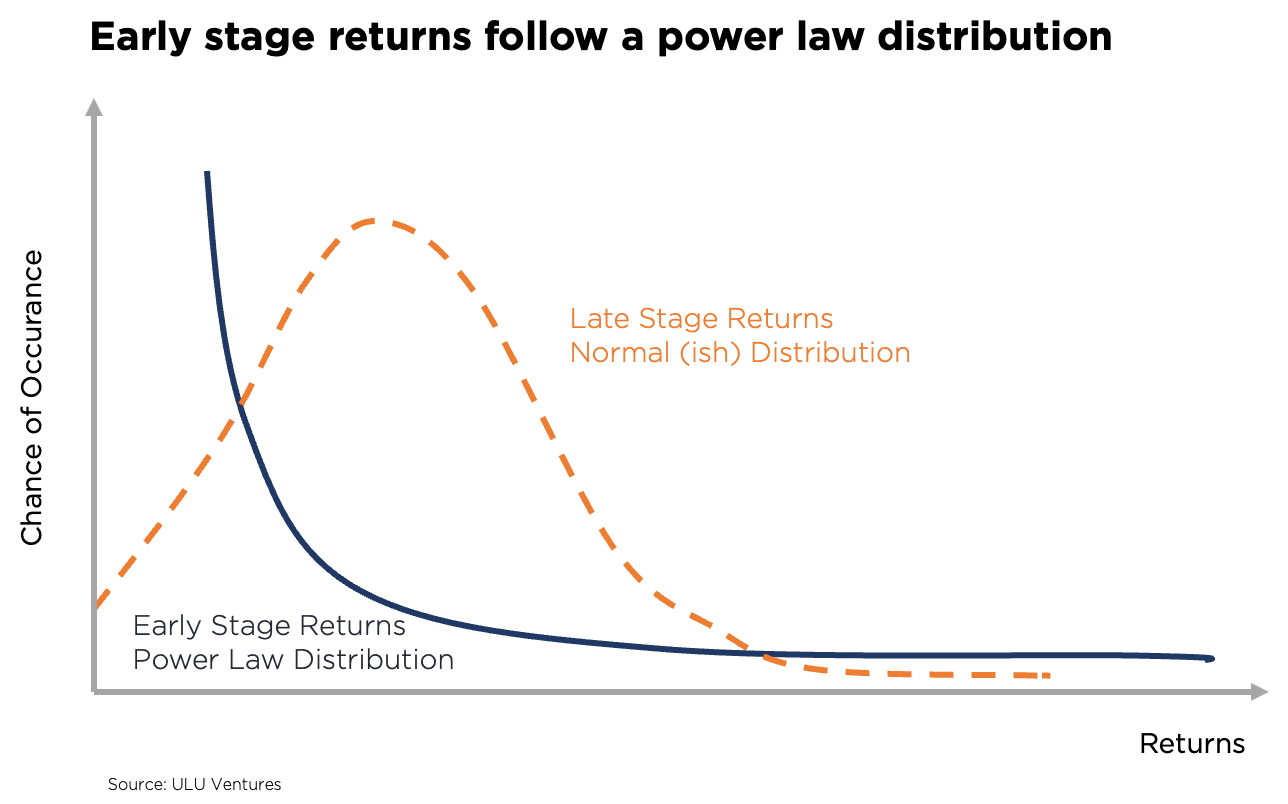

The power law hasn't been repealed

More than 50 years of venture data tell a remarkably consistent story. Across every technology paradigm, from PCs to the internet to mobile to SaaS and now AI, one pattern has never broken: a tiny number of investments produce nearly all the returns.

The steepness of that power law has shifted over the decades, but the most important statistic has stayed stable. Roughly one in 100 investments returns an entire fund, and more than 90% of funds returning 3x or more had at least one of those fund returners. Without one, the likelihood of delivering 3x net DPI to LPs falls dramatically.

The implication for portfolio construction is simple. Until the data says otherwise, your portfolio needs to be built to maximize your chance of landing a fund returner. No evidence yet suggests that AI has changed this; so far, we have only arguments that it might do so.

Five inputs AI may be shifting

Where things are changing is in the inputs that feed portfolio construction decisions. Five shifts stand out:

1. Revenue ramps are compressing. AI companies are reaching $1M in ARR in under a year and $100M in roughly four years, about three times faster than the SaaS benchmarks many investors built their intuitions on.

2. Gross margins are bifurcating. The fastest-scaling AI companies, prioritizing customer acquisition over margins, are averaging just 25% gross margins, while those that grow more steadily like strong SaaS businesses are maintaining gross margins around 60%. Meanwhile, VC practitioners are split in their views: one camp expects margins for the fastest growers to recover toward SaaS levels as model and inference costs fall, while the other camp sees AI margins as structurally lower, since every query carries a real compute cost that optimization can shrink but not erase.

3. Retention is splitting by price point. AI products under $250/month ACV are seeing heavy churn, while enterprise AI companies past $10M ARR are often posting net retention above 100%, in line with or better than traditional B2B SaaS.

4. Capital is concentrating. The top 10% of US startups raised half of all VC investment last year, and in the first quarter of this year, just four companies accounted for nearly two-thirds of all global venture funding.

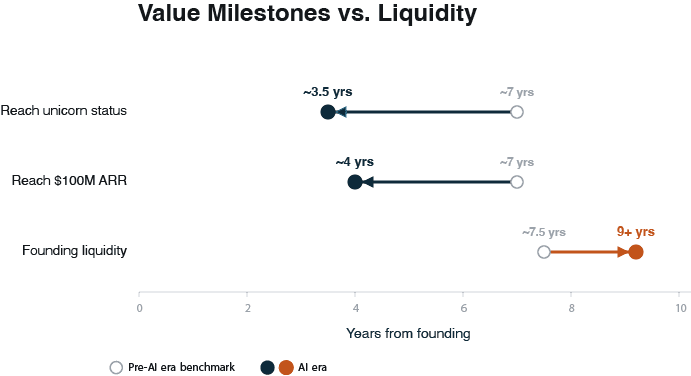

5. Valuation mark-ups on paper are arriving faster. AI startups are reaching unicorn status in about three and a half years, far faster than previous sectors.

The liquidity conundrum

Here's the catch, and it may be the most important tension in venture today: despite everything speeding up, time to exit has not. The journey from founding to liquidity now averages over nine years.

Sources: ValueaddVC, BVP, Pitchbook

Companies are getting valuable faster, but they aren't getting liquid faster. For emerging managers, that creates a strategic conundrum: are you managing for TVPI, the strong paper marks that help you raise your next fund, or for DPI, the actual distributions you eventually deliver to your LPs? Too many emerging VC fund managers haven't fully thought through this distinction, and being out of sync with what your LPs actually want can quietly undermine an otherwise strong track record.

Pressure on the classic levers

These shifting inputs put real pressure on the traditional levers of portfolio construction.

Reserve strategies are getting squeezed. While median company now takes roughly two years to go from seed to Series A, the hottest AI names compress that timeline to under a year and often only a few months. For investors chasing those fast movers, the risk is getting priced out of their pro rata before their reserves ever come into play. Meanwhile, the minimum viable fund size may also be rising. With median post-money valuations for AI seed rounds around $25M, buying meaningful ownership is getting harder for the smallest funds.

The longstanding debate between concentration and diversification is also being reframed. One useful lens: horizontal AI plays may favor concentration, since the exits are enormous but few, while vertical AI may favor diversification across a larger population of companies with higher failure rates.

Maybe the fund vehicle is the problem

There's also a more provocative school of thought worth considering: perhaps the answer isn't better portfolio construction math at all. Some practitioners argue that the standard venture fund vehicle itself is the outdated piece. A 10-year closed-end fund with capital committed up front was built for an era of smaller funds and a shorter, more predictable seed-to-IPO path, and neither still holds. Under this view, the real opportunity for newer managers is rethinking fund structure, possibly through evergreen or shorter-cycle vehicles, or by financing companies deal by deal rather than around a fixed fund life.

The bottom line

What hasn't changed is that the power law still rules, fund returners still determine top-quartile outcomes, and vintage-year luck is usually only visible in hindsight. What may be changing is nearly every input that feeds the portfolio construction model.

Nobody knows yet where this is heading. The most honest approach is to watch the data closely while building a coherent strategy you can deviate from deliberately, rather than drifting deal by deal into ad hoc allocations. In a market where every input is in motion but the expected outputs of LP return multiples and liquidity timelines stay the same, the durable edge isn't a sharper forecast; it's the discipline to build and execute an allocation strategy, paired with the judgment to know when to break it. That is why a working command of portfolio construction matters more now, not less. The managers who understand how the levers actually interact, from reserves and ownership to concentration and pacing, are the ones who will succeed under real uncertainty.

These insights come from our recent webinar with Trevor Loy of Flywheel Ventures, a Stanford lecturer and longtime VC Unlocked faculty member, where he unpacked the data behind each of these shifts, including 50 years of power law charts and the live debates among leading VC practitioners. Watch the full conversation here: https://events.500.co/portfolio-construction-ai-unit-economics

Learn more about VC Unlocked: Silicon Valley, taking place at Stanford University on August 24 - September 4, and secure a nomination to join this year’s cohort.